In setting our investment strategy, we seek to act in the best financial interests of the Fund, our members and our stakeholders, pursuing the best return that is consistent with a prudent and appropriate level of risk. We will consider material environmental, social and governance (ESG) issues where they are likely to affect the value of our investments or potential investment opportunities, especially over the long-term. We consider this a prudent approach to investment and risk management.

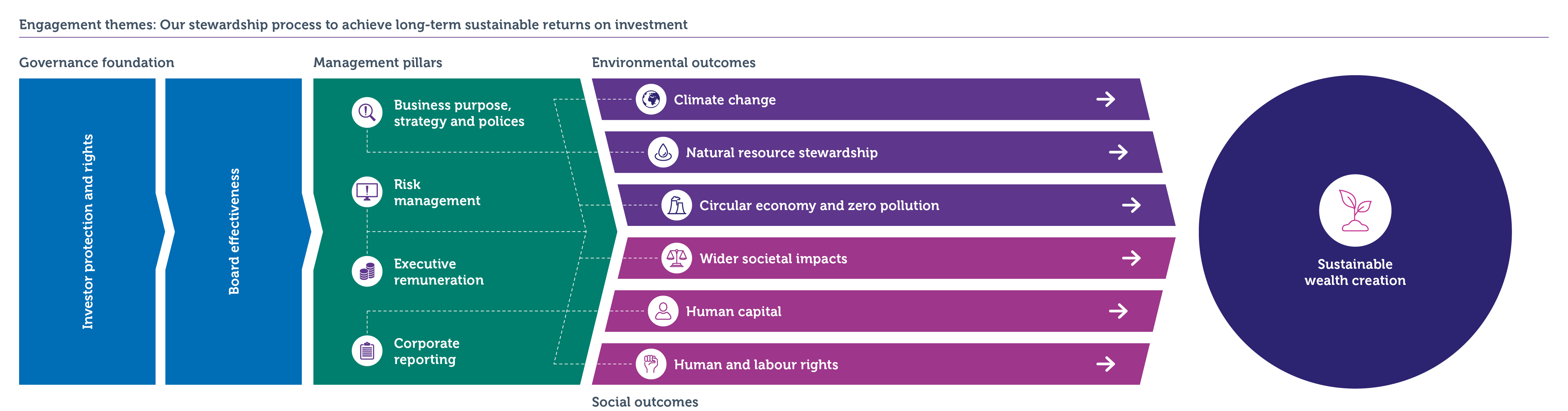

In line with the PPF’s Sustainability Policy, we believe that good corporate governance and management of ESG risks goes hand in hand with good risk management overall. In particular, consistent mishandling of ESG issues can be an early indicator of wider management or financial problems yet to emerge, and can impact the stability of capital markets, alongside more dominant factors such as issuer or market level liquidity. Active ownership through purposeful dialogue, utilising the use of our votes and engagement, is a key part of our role as a responsible asset owner.

We are committed to exercising our ownership rights, in order to safeguard sustainable returns for the Fund in the long-term. The PPF, or agents operating on our behalf, will demonstrate active ownership as part of our oversight role, through decisions around portfolio construction, access to company management, and voting on matters such as capital structure, risk management, strategy, financial performance, social and environmental issues - including climate change - and corporate governance. We see this as an essential means of ensuring that boards are accountable and that are fulfilling their stewardship obligations to key stakeholders (including but not limited to shareholders), in order to deliver long-term value.

The PPF recognises the good practice set out in the UK Stewardship Code 2026, and supports the principles underpinning the UK Corporate Governance Code 2024, while also acknowledging best practice or standards in other markets, both in and outside of the UK, across various asset classes. The United Nations-supported Principles for Responsible Investment (PRI) form a core element of our own RI approach, including Principle 2: we will be active owners and incorporate ESG issues into our ownership policies and practices, Principle 5: we will work together to enhance our effectiveness in implementing the Principles and the more recently published PRI’s Active Ownership 2.0. We also support the broader context of stewardship as defined by the International Corporate Governance Network (ICGN) Global Stewardship Principles that effective stewardship enhances overall financial market stability and economic growth.

The PPF’s RI strategy puts our core RI beliefs into practice through a robust RI framework as follows:

Stewardship sits as one of our three key priorities within our RI framework. We take a blended approach across several aspects regarding the oversight and implementation of stewardship at the PPF, dependent on how the assets are managed. This includes the selection of fund managers, the setting of mandate-specific parameters (such as segregated versus pooled investments), and the agreement about how stewardship will be carried out (e.g. in-house by the PPF, or through the external fund manager or third-party provider).ESG integration across the Fund is achieved by engaging with our internally managed assets, our external fund managers and their underlying issuers. As a large and diversified asset owner, we have the opportunity to encourage improvements in practices from the top down and bottom up. This is particularly important when looking to address systemic issues and achieve outcomes at the market-wide level, for example the transition to a low-carbon world. We primarily believe in engagement over divestment, as a fundamental enabler to the objective of achieving more sustainable outcomes.

We have a minimum standards policy that stipulates a certain level of responsible conduct from our underlying issuers, and seek to avoid investing in issuers that contravene this. This policy is aligned with international conventions or norms for controversial activities that are ratified into UK law, for example the production of specific controversial weapons.

As an investor with holdings in both corporate equities and debt, we believe it is important to consider both the shareholders and creditors as providers of corporate capital, in stewardship activities. We also believe that good stewardship practices should be applied to other asset classes aside from listed equities and corporate debt (such as private debt, private equity, real estate and infrastructure), although the level of control or influence and how it impacts stewardship may lead to differing approaches by asset class or strategy.