We've confirmed a zero levy for conventional schemes for 2026/27. For more information about this change, view our announcement and FAQs.

Our levy webpages will be updated in due course after the 31 March 2026, in line with the 2026/27 levy rules taking effect.

Our levy webpages will be updated in due course after the 31 March 2026, in line with the 2026/27 levy rules taking effect.

How we calculate the levy

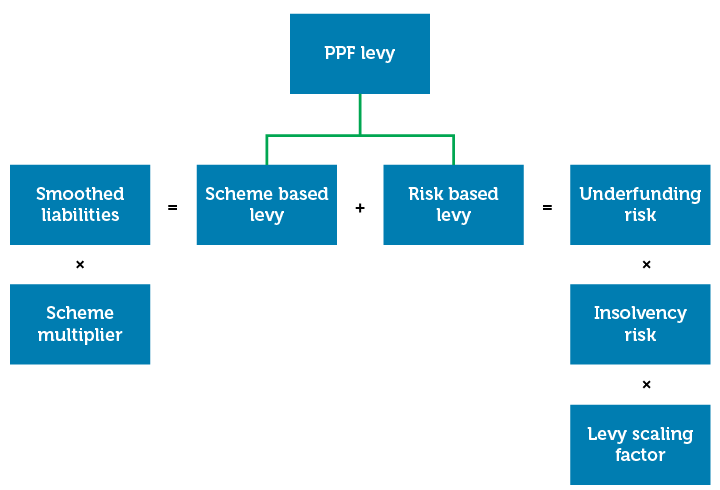

How we calculate the scheme-based levy

It’s calculated using your scheme liabilities, as reported in the most recent s179 valuation on the Regulator’s Exchange system at 31 March immediately preceding the levy year being calculated.

All scheme liabilities are rolled forward to a common date of 31 March in the current year.

Liability figures are smoothed over a five year period but not stressed. We then apply the scheme-based multiplier to this value.

How we calculate the risk-based levy

This is calculated by reference to the likelihood of an insolvency of the scheme employer and the potential size of the claim that might be passed on to us.

The potential size of the claim is based on the s179 valuation information that you submit to The Pensions Regulator, which is then adjusted.

These adjustments have three objectives:

- To make sure different schemes’ funding is on a common basis

- To smooth year-to-year movements in funding

- To take account of investment risk

The likelihood of the scheme employer becoming insolvent is based on that employer’s insolvency risk score.

If your scheme doesn't have a deficit on our basis then you won't have to pay this levy.

To learn more about your risk score, read about providing insolvency risk information and access our portal to check your employer scores and data used for scoring.

Protecting the most vulnerable schemes

We cap the risk-based levy to help protect the most vulnerable schemes. This means that the maximum risk-based levy a scheme can be charged is 0.5 per cent of their unstressed liabilities.